Before You Choose Medicare, Start With These Three Questions

"My friend said I should choose a Medicare Advantage plan. Do you think that's what I should do?"

A client asked me that question in a recent meeting. She had already enrolled in a Medicare Advantage plan because a friend recommended it. Her friend told her what she liked about it and suggested it may be good for her too.

The recommendation wasn't bad, it just wasn't based on my client’s retirement.

As we discussed her travel plans and the flexibility to see physicians in different parts of the country the conversation shifted from "Which plan is best?" to "What do you want retirement to look like?", the answer became much clearer. Original Medicare paired with a Medigap policy would likely be a better fit for the retirement my client wanted.

Fortunately, it wasn't too late to make a change.

That conversation reinforced something I've found to be true over the years, the best Medicare decisions don’t start with Medicare—they start with retirement.

We Start with Retirement

One of my favorite moments in a planning meeting is when someone realizes we've been talking for twenty minutes about Medicare...without actually talking about Medicare.

Most people expect us to begin by explaining Parts A, B, C, and D but we usually don't. Instead, we start with questions.

- Will you continue working after age 65?

- When do you want to retire?

- What do you want retirement to look like?

- Do you expect to travel often?

- Are there doctors you want to continue seeing?

- Will you still be contributing to a Health Savings Account? (That question surprises people more often than you'd think.)

Those answers tell us far more than your birth date ever will.

Someone planning to retire at 65 may have very different options than someone planning to work until 68. Someone who spends winters in Arizona and summers in South Carolina may value healthcare flexibility differently than someone who plans to stay close to home. We want to understand the life Medicare is supposed to support.

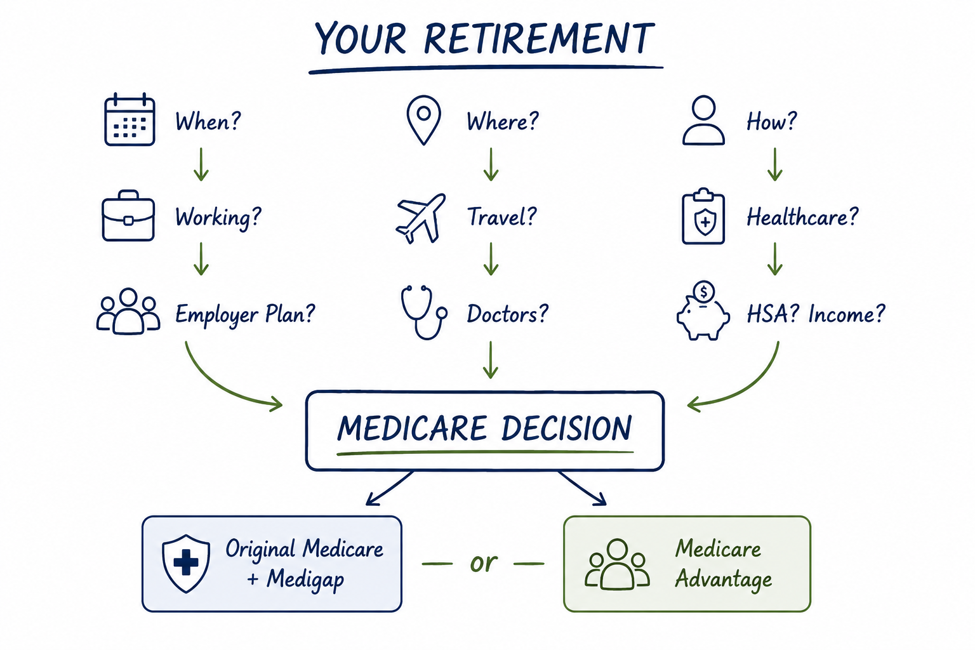

Your Life → Your Coverage

Before recommending a Medicare strategy, here's how we think about the conversation:

Notice what's at the top, it’s not Medicare, it’s your retirement, that's intentional.

A Simple Way to Think About Medicare

Once we understand your situation, Medicare becomes much easier to explain.

Think of Part A as your hospital coverage. If you're admitted to the hospital, Part A is generally where your Medicare coverage begins.

Part B covers most of what happens outside the hospital: your primary care physician, specialists, outpatient care, and what I often think of as your ongoing healthcare maintenance.

Part D helps cover prescription medications.

You'll notice I skipped Part C, that wasn't an accident.

Part C, or Medicare Advantage, is another way to receive your Part A and Part B benefits through a private insurance company. Most Medicare Advantage plans also include Part D prescription drug coverage and may offer additional benefits such as dental, vision, or hearing coverage.

Don't worry about memorizing the alphabet soup. Understanding what each letter does is helpful, but it's rarely what determines whether someone makes a good Medicare decision.

The Three Decisions That Really Matter

Once people understand the basics, I encourage them to think about three questions.

- Do I need to enroll right away?

Many people assume turning 65 automatically means enrolling in Medicare and sometimes that's true but sometimes it isn't.

If you're still working and covered by a qualifying employer group health plan, you may be able to delay enrolling in certain parts of Medicare without penalty. Whether that's appropriate depends on factors such as your employer coverage and your specific circumstances.

The important thing is understanding which rules apply to your situation before making a change.

- Which type of coverage fits my retirement?

This is where you'll compare Original Medicare, Medigap, and Medicare Advantage. Notice we aren’t looking to find "Which plan is best?" We’ve found there usually isn't a universally "best" Medicare solution. There's only the solution that best supports the retirement you're trying to build.

For some people, that's Medicare Advantage, for others, it's Original Medicare paired with a Medigap policy. The right answer depends on much more than the insurance itself.

- How does Medicare fit into everything else?

This is the question I think gets overlooked most often. Your Medicare decision may affect, or be affected by, your HSA contributions, retirement cash flow, tax planning, future Roth conversion opportunities, and how easily you can access healthcare while traveling. Those aren't just Medicare decisions, they're retirement decisions.

And that's why we believe Medicare deserves to be a part of the comprehensive retirement plan, not a separate conversation after everything else has already been decided.

Questions We'd Ask Before Making a Recommendation

Before recommending any Medicare strategy, we want to understand:

When do you plan to retire?

Will you continue working?

What health insurance do you have today?

What do you want retirement to look like?

Will you travel frequently?

Are you contributing to an HSA?

Are there doctors or healthcare systems you want to continue using?

How important is flexibility if your health needs change over time?

Did you notice that only a few of those questions are actually about Medicare. Most of them are about you and the life you’re building. That's intentional because in our experience, once we understand your life, the Medicare decision usually becomes much clearer.

One More Thing to Think About

People often spend weeks researching Medicare plans before spending ten minutes thinking about what they want retirement to look like, we recommend reversing that.

Take the time to define the retirement you're trying to build first. Then choose the Medicare coverage that supports it.

Your friend may have made exactly the right decision, your neighbor may have too, the question isn't whether their decision was right, the question is whether it's right for your retirement.

The best Medicare decision isn't the one someone else recommends, it's the one that helps you live the retirement you've worked so hard to achieve.

Medicare.gov – Your Coverage Options

- Explains Original Medicare, Medicare Advantage (Part C), Part D, and Medigap.

- https://www.medicare.gov/basics/get-started-with-medicare/get-more-coverage/your-coverage-options

Social Security Administration – When to Sign Up for Medicare

- Initial Enrollment Period, employer coverage, and delayed enrollment considerations.

- https://www.ssa.gov/medicare/plan/when-to-sign-up

CMS – Medicare Managed Care Eligibility and Enrollment

- Technical guidance on Medicare Advantage eligibility and enrollment.

- https://www.cms.gov/medicare/enrollment-renewal/managed-care-eligibility-enrollment

Disclosure: The information provided in this blog post is for educational and informational purposes only and should not be construed as financial advice. While we strive to present accurate and up-to-date information, the financial, tax, and legal landscape is subject to change, and individual circumstances vary. Readers are encouraged to consult with a qualified financial advisor or professional before making any financial decisions or implementing strategies discussed in this post. Our firm does not guarantee the accuracy, completeness, or suitability of the information provided, and we disclaim any liability for any direct or indirect damages arising from the use of this information. Artificial Intelligence was used to assist in the writing of this article. Past performance is not indicative of future results. Any investment involves risk, and individuals should carefully consider their financial situation and risk tolerance before making any investment decisions.